Aircraft brake procurement is governed by qualification standards that create market structures unusual even within aerospace. Once a brake manufacturer achieves FAA and EASA Part Manufacturer Approval for a specific brake part number on a specific aircraft type, that approval covers both the OEM installation and aftermarket MRO replacement market for that brake on that aircraft for the duration of its production and service life. Competing against a PMA-qualified brake supplier requires either matching their qualification investment or competing on price within the same approved design, making technical qualification depth the primary competitive credential in this market. The intelligence needed to understand how that qualification coverage is distributed, where gaps exist in the competitive landscape, and where new program approvals will generate revenue is the core analytical requirement for commercial strategy in this sector. The Aircraft Brake Market Report published by The Insight Partners delivers that intelligence with full segmentation analysis, five-region coverage, and SWOT profiles for each of the ten key companies through the confirmed 6.6% CAGR to 2031.

The study covers the 2025 to 2031 forecast period with historic data from 2021 to 2023 and 2024 as the base year, providing country-level market sizing across both segmentation dimensions in all five world regions.

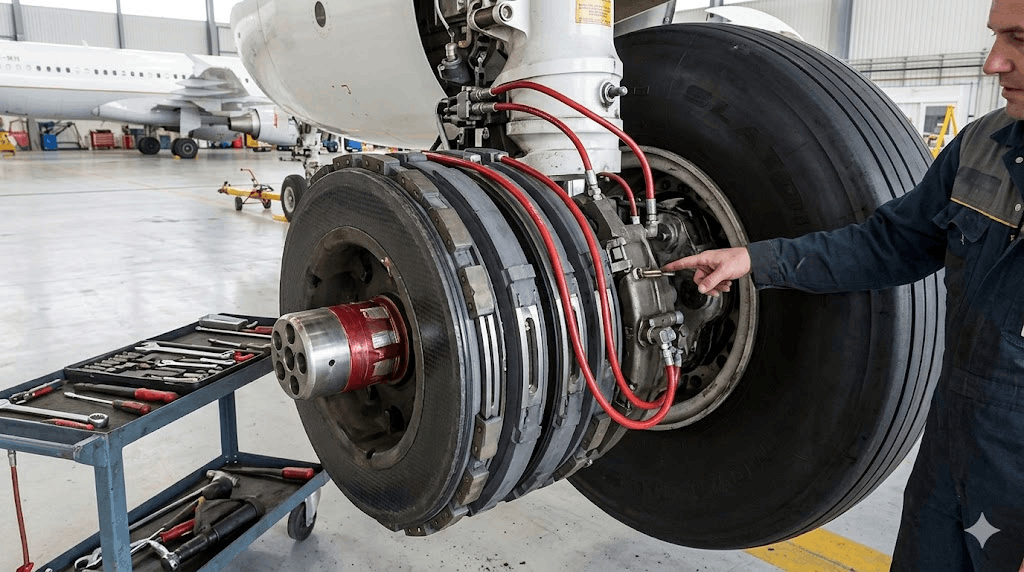

Get exclusive insights into the Aircraft Brake Market – https://www.theinsightpartners.com/sample/TIPRE00004965

The dual-lens demand and supply methodology examines how fleet production, MRO expansion, electric brake adoption, and next-generation aircraft programs translate into brake procurement demand across each type and end-user segment in each regional market. The demand lens separately models OEM production program demand, MRO replacement demand, and technology upgrade demand from electric brake transition as three procurement channels. The supply lens examines competitive positions, PMA and type certificate qualification coverage breadth, carbon brake material technology capability, electric brake development programs, and MRO service network depth across the ten profiled companies. PEST analysis contextualizes each region's commercial aviation production and fleet growth trajectory, military aircraft procurement environment, and aviation regulatory certification framework.

Competitive Landscape

- AVIATION BRAKE SERVICE INC.

- Bauer, Inc

- Collins Aerospace

- Crane Aerospace and Electronics

- Honeywell International Inc.

- Lufthansa Technik AG

- Matco Manufacturing Inc.

- Meggitt Plc.

- PARKER HANNIFIN CORP

- Safran SA

Q1. What confirmed market trajectory and CAGR does the aircraft brake market report establish?

The market grows from US$ 9.10 billion in 2024 to US$ 14.24 billion by 2031 at a confirmed 6.6% CAGR as published by The Insight Partners, with country-level sizing across both segmentation dimensions in all five world regions.

Q2. What three demand channels does the report model within the aircraft brake market?

OEM production program demand for line-fit brake installation, MRO replacement demand from the global in-service fleet reaching brake service life limits, and technology upgrade demand from electric brake system adoption on new-generation aircraft programs are the three separately modeled procurement channels.

Q3. Why is PMA and type certificate qualification coverage breadth a primary supply lens dimension?

FAA PMA qualification creates approved supplier status for specific brake part numbers on specific aircraft types, making qualification breadth directly determinant of addressable market scope, with competitors unable to supply approved brake components for aircraft types outside their qualification portfolio regardless of product quality or price competitiveness.

Q4. What PEST dimensions are most commercially significant for the aircraft brake market?

Commercial aircraft production rate trajectories affecting OEM demand volume, global commercial fleet MRO market development affecting aftermarket demand, military aviation procurement programs affecting defense brake demand, FAA and EASA qualification certification framework affecting PMA approval timelines, and aviation safety regulatory advancement affecting brake performance standards are the most commercially significant PEST dimensions.

Q5. Who benefits most from the aircraft brake market report intelligence?

Aircraft brake manufacturers gain segment and geographic demand mapping for qualification investment and market entry decisions. Airlines and MRO operators receive technology trajectory and supplier landscape intelligence for brake procurement planning. Aerospace investors receive validated market trajectory and competitive structure analysis for capital allocation in the aviation supply chain.

About The Insight Partners

The Insight Partners is a one-stop industry research provider of actionable solutions. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media and Telecommunications, Chemicals and Materials.

Contact Us

The Insight Partners

Phone: +1-646-491-9876

E-mail: sales@theinsightpartners.com